According to a May 2013 report by the non-profit Council for Disability Awareness (CDA), there is a sharp mismatch between the high value employees place on their ability to earn a living vs. their financial preparedness to handle a disability that would threaten their income as evidenced by having adequate levels of disability insurance.

According to a May 2013 report by the non-profit Council for Disability Awareness (CDA), there is a sharp mismatch between the high value employees place on their ability to earn a living vs. their financial preparedness to handle a disability that would threaten their income as evidenced by having adequate levels of disability insurance.

Most are Ignorant of the Real Need for Disability Insurance

The report titled “Disability Divide: Employer Study” is based on a 2012 survey of over 500 human resources professionals. The key findings, as reported by the Insurance Word Blog, are as follows:

- ¾ of HR professionals surveyed said employees viewed their income-earning ability as their most valuable financial resource, ahead of medical insurance, their homes, and retirement savings. However, only ¼ said employees considered it “very important” to prepare for potential disability, and a similar portion felt their employees were prepared to handle the financial hardships of the loss of income due to illness or injury.

- A prior CDA survey of over 1,000 wage earners yielded similar results, with most respondents stating they are most likely to agree with the statement, “I never really thought about” preparing for a potential disability.

- The HR experts surveyed generally felt that employees should begin planning for disability early in their careers even though most don’t begin until age 40 or older, if ever. According to statistics, approximately 100 million members of the US civilian workforce have no private disability insurance.

- Most of the HR experts as well as the wage earners dramatically underestimated the likelihood of incurring a disability during their careers.

Surprising Disability Insurance Statistics

The post goes on to quote some surprising statistics from the CDA’s Personal Disability Quotient calculator:

- An average 35-year old male office worker who is a non-smoker and has no health history issues has a 13% risk of incurring a long-term disability prior to retirement.

- For women with the same profile the risk is higher: 18% or nearly 1 in 5. Those surveyed had estimated their risk at only 1-2%.

- The 35-year olds noted above, if earning an average of $50,000 per year, are likely to earn approximately $2.4 million on average by the end of their careers.

- Clearly, the contrast between the risk of losing millions in income and the lack of disability insurance is striking!

Key Takeaways

Americans are much less protected against income loss than in the past due to several factors, including:

- The relative lack of solid pension plans

- Much lower savings rates

- Home mortgages with higher balances

- Rising college education costs

- Given the poor economy, the much greater likelihood of the need to continue to support children beyond their college years

What to do About Disability Insurance

Given these facts, the only wise course of action is to acquire the proper level of disability insurance to cover the gap between your current savings and the funding that would be needed to cover your financial needs during a long-term disability. If you are a business owner, the risks of inadequate disability insurance may be even greater due to the financial consequences of being unable to work.

We’re Here to Help if Needed

If you have questions on how to determine the right level of disability insurance you need to protect both you and your loved ones, then please contact us at 610-947-1270, or Contact Us online.

Tags:

Health Insurance Reading PA,

Health Insurance Allentown,

Health Insurance Harrisburg,

Small Business Insurance,

Disability Insurance,

Health Insurance,

Health Insurance Berks County,

Health Insurance Philadelphia,

Health Insurance Lancaster

GAP insurance refers both to Guaranteed Asset Protection and Guaranteed Auto Protection. In both cases it is designed to cover the difference (or gap) between the actual cash value of an asset and the amount still owed on the related loan or lease. While, strictly speaking, GAP insurance may apply to any type of asset, the vast majority of GAP insurance policies are written for cars, trucks, vans, and other types of vehicles.

Why Bother With GAP Insurance?

GAP insurance may be a wise choice in cases where a low down payment has been made, and on high-interest loans of 60 months or more. It is often offered by finance companies at time of purchase, and by auto insurance companies. This loan scenario frequently applies to vehicle purchases, which is why the term “GAP insurance” most often refers to added insurance protection for a vehicle.

GAP insurance may be a wise choice in cases where a low down payment has been made, and on high-interest loans of 60 months or more. It is often offered by finance companies at time of purchase, and by auto insurance companies. This loan scenario frequently applies to vehicle purchases, which is why the term “GAP insurance” most often refers to added insurance protection for a vehicle.

GAP Insurance Considerations When Buying a New Car or Other Vehicle

Cars, trucks, motorcycles and other vehicles are assets that depreciate rapidly in value. In cases where a low down payment is made on the initial purchase, it is common for the amount remaining on the loan to exceed the fair value of the car. This is because cars often lose up to half their retail within 3 years from the purchase date, at which time the remaining loan may far exceed that amount. If your car becomes stolen or is totaled, the replacement value you receive from the insurance company may be far less than the amount remaining on the loan. In such cases a GAP insurance policy would cover the difference. If you would be unable to cover the difference without GAP insurance in such cases, or if this would represent a significant financial hardship, then GAP insurance may be right for you.

How to Get GAP Insurance for Your Vehicle

GAP insurance may be purchased from an insurance agent or through a car dealership. GAP insurance coverage is often financed as part of the loan or lease, and typically comes into play when a vehicle is subject to a total loss. Some finance companies require GAP insurance when financing a loan.

How to Save on GAP Insurance

We suggest checking first with your independent insurance agent before signing a GAP policy related to a vehicle purchase. Your independent agent may be able to save you money by adding this coverage to your vehicle insurance policy rather than taking out a separate policy through your car dealership. To learn more about getting the right GAP Insurance for your vehicle, call us at 610-775-3848 or use the Contact Us form.

GAP Insurance for Your Business

When it comes to insuring your business “GAP insurance” refers to Guaranteed Asset Protection, and often comes in the form of a “guaranteed replacement cost” or “agreed value” insurance policy. In such cases your business property is insured for an amount that is guaranteed in advance regardless of what the market value may be at the time of your claim. This speeds the time to settle your claim, and may help you sleep better at night.

To learn more about the many commercial insurance options for your business, call us at 610-775-3848 or use the Contact Us form.

Tags:

Car Insurance Harrisburg PA,

Car Insurance Lancaster PA,

Affordable Motorcycle Insurance,

Car Insurance,

Car Insurance Reading PA,

Car Insurance Allentown PA,

GAP Insurance,

Car Insurance Philadelphia PA,

Affordable Car Insurance

Have you recently started a new business, or perhaps suddenly come to the realization that your personal vehicle insurance may not fully protect you when using your car, van, or truck for business purposes?

Commercial Vehicle Insurance Coverage Differs by Company

Although each insurance company has different guidelines for determining to what extent your personal vehicle may be insured when used for commercial purposes, it is nonetheless risky to assume your personal vehicle will be properly covered, if it is covered at all. Rather than taking chances, consult an independent insurance agent to learn the details of your coverage, and to select the best insurance company and policy to meet your commercial insurance needs.

Although each insurance company has different guidelines for determining to what extent your personal vehicle may be insured when used for commercial purposes, it is nonetheless risky to assume your personal vehicle will be properly covered, if it is covered at all. Rather than taking chances, consult an independent insurance agent to learn the details of your coverage, and to select the best insurance company and policy to meet your commercial insurance needs.

How to Know if Your Vehicle Use is Commercial or Personal

The most obvious indicator that you are using your vehicle for business purposes occurs when you are using your car, van, truck, or other vehicle to transport merchandise or people, or to perform services for a fee.

For example, if you are using your vehicle to:

- Deliver flowers or restaurant food, such as pizza or other food items

- Perform landscaping services, such as delivering workers and/or materials

- Perform snow removal services

- Tow a trailer used for business purposes

- Travel to customers for sales calls or to perform consulting services

Who is Covered Under a Commercial Vehicle Insurance Policy?

Unlike a personal policy, commercial vehicle policies allow you to cover any of your employees when your vehicle is used for business purposes. If your vehicle is driven by employees, that’s a sure sign that you need a commercial policy. Likewise, if your vehicle is owned under a corporate partnership, or used to haul heavy equipment, or to make deliveries requiring federal or state filings, then you definitely need commercial vehicle insurance protection.

Amount of Vehicle Insurance You Need for Business vs. Personal Use

Commercial vehicle insurance policies generally provide greater protection than personal policies, with higher liability limits. However, it’s very important to make sure you are fully protected for both business and personal use if your vehicle is used for both.

Don’t Take Chances!

By now we hope you are thoroughly convinced that it is not worth taking chances with your commercial vehicle insurance coverage. Whether you hail from a larger city like Philadelphia or Allentown, or smaller areas like Reading or Lancaster, you need the right insurance protection. Please don't take chances with your future.

To learn more about commercial insurance for your car, van, truck, or commercial fleet, click here. Or, contact us online. You may also reach us at (610) 775-3848. We’re independent insurance agents who stand ready to help you find the insurance protection that’s right for you, your budget, and your business.

Tags:

Van Insurance,

Commercial Vehicle Insurance,

Business Insurance Reading PA,

Business Insurance Berks,

Business Insurance Philadelphia Pa,

Business Insurance Lancaster Pa,

Business Insurance Harrisburg Pa,

Business Insurance York Pa,

Commercial Insurance Allentown PA,

Commercial Insurance Lancaster PA,

Commercial Insurance Harrisburg PA,

Commercial Insurance,

Commercial Insurance Reading PA,

Business Insurance Allentown PA,

Business Insurance,

Commercial Insurance Philadelphia PA,

Commercial Insurance York PA,

Commercial Insurance Berks County

Chances are that your current homeowner’s insurance policy is weaker than you think in terms of the financial protection it offers. That’s because many insurers have been steadily changing their coverage to increase deductibles and to add new loopholes protecting the insurance company from excessive loss. To make matters worse, homeowner’s insurance rates have climbed 69% over the past 10 years and now average approximately $1,000 per year.

Why the Big Homeowner’s Insurance Cost Increases?

Why the Big Homeowner’s Insurance Cost Increases?

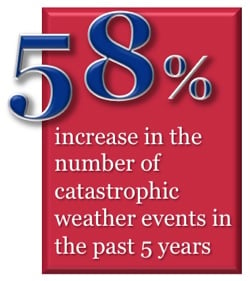

So why are insurers raising home insurance rates, cutting coverage, and increasing deductibles in Reading, Philadelphia, Allentown, Lancaster, and all across Pennsylvania and the US? Is it nothing more than unbridled greed? Hardly. Insurers are experiencing factors beyond their control that are driving up costs. The biggest factor alone, the weather, has resulted in a 58% increase in the number of catastrophic weather events in the past five years vs. the prior five, climbing from 602 to 953 according to insurance industry data. Of course, along with each disaster comes a series of insurance industry payouts to policy holders.

Another factor driving these changes is that states have denied insurers’ requests to increase their rates to the full extent needed to capture the true increases in weather-related payouts. As a result, insurers have resorted to shifting a much larger percentage of the cost of homeowner’s claims to their customers in an effort to remain solvent, and this has been done by cutting coverage. Many homeowners are on the hook for far more of the cost of repairs than they were five years ago. Homeowner’s insurance is among the least profitable forms of insurance, and, as they say, you can’t get blood from a rock, so something has to give, and that has been both the extent and cost of coverage.

Get Help: Homeowner’s Insurance Coverage Varies Widely

Because house insurance coverage varies widely among insurers, and given that the specifics of what is covered and what is not are often buried in the insurance policy fine print, it is wise to seek the advice of an independent insurance agent to help you make sense of the coverages, deductibles, and loopholes within policies offered by various insurance carriers. An independent agent is uniquely positioned to help you find the best policy for your needs and budget because he or she represents multiple competing carriers, rather than just one. Don’t rely solely on an insurance company’s reputation or marketing. Instead get the facts so you can make an informed purchase.

Because house insurance coverage varies widely among insurers, and given that the specifics of what is covered and what is not are often buried in the insurance policy fine print, it is wise to seek the advice of an independent insurance agent to help you make sense of the coverages, deductibles, and loopholes within policies offered by various insurance carriers. An independent agent is uniquely positioned to help you find the best policy for your needs and budget because he or she represents multiple competing carriers, rather than just one. Don’t rely solely on an insurance company’s reputation or marketing. Instead get the facts so you can make an informed purchase.

We Can Help

Are you and your family in a precarious position? Arrange for a homeowner’s insurance review with an independent agent. Why not make an appointment today? You’ll sleep better knowing you did the smart thing. Call us at (800) 947-1270 or (610) 775-3848, or click below to contact us.

Tags:

House Insurance Reading PA,

Homeowners Insurance Lancaster Pa,

House Insurance Allentown Pa,

House Insurance Lancaster Pa,

Homeowners Insurance Philadelphia Pa,

House Insurance,

Homeowners Insurance,

Homeowners Insurance Allentown Pa,

Homeowners Insurance Reading Pa,

House Insurance Philadelphia Pa,

Homeowners Insurance Harrisburg PA,

Homeowners Insurance York PA

If you are a landlord and you have tenants leasing your commercial property, you may want to take a second look at your lease agreement. You may also want to review your landlord insurance policy to make certain the two are in harmony. Failing to do so may result in unexpected costs, lack of insurance protection, or coinsurance hassles in the event of a claim.

Whose Commercial Insurance Policy Pays for Damage to Improvements?

As the owner of a commercial building, any permanent upgrades made to your property by a tenant become your property, not the tenant’s property. This may seem obvious, but consider the impact should damage be done to such improvements during the tenant’s leasing period. Whose insurance will pay for the repair or replacement cost? Will either insurance policy pay? Will both pay? Can you live with the uncertainty of not knowing?

As the owner of a commercial building, any permanent upgrades made to your property by a tenant become your property, not the tenant’s property. This may seem obvious, but consider the impact should damage be done to such improvements during the tenant’s leasing period. Whose insurance will pay for the repair or replacement cost? Will either insurance policy pay? Will both pay? Can you live with the uncertainty of not knowing?

Getting it Right When You Craft the Lease Agreement

As a commercial property owner, you should clearly define who is liable for replacing or repairing permanent improvements and upgrades that become damaged. Even though the tenant’s commercial insurance policy normally covers damage to permanent improvements made by the tenant, it may be unwise to put the responsibility exclusively on the tenant. Here’s why: if the owner takes responsibility then he can include the value of the improvements in the policy limit, thereby avoiding coinsurance penalties.

Did Your Tenant Opt Out of Insuring Permanent Improvements?

If the tenant does not want to insure the improvements, he can exclude such coverage via an Additional Property Not Covered endorsement. Furthermore, it is possible that even though the tenant has insurance for improvements, he may be underinsured. Finally, if your lease has an early termination provision allowing the owner to cancel the lease if the building is significantly damaged, then the tenant’s policy will not cover the loss.

Ignorance is Dangerous When it comes to Commercial Property Insurance

The scenarios above should make it clear that ignorance of the details of your lease agreement and your commercial insurance policy can be dangerous to your financial health. The two should be in harmony, especially when it comes to covering permanent improvements made by the tenant.

Please call us at (610) 775-3838 if you would like help in obtaining the proper landlord insurance protection for your rented commercial property.

Tags:

Business Insurance Reading PA,

Business Insurance Berks,

Business Insurance Philadelphia Pa,

Business Insurance Lancaster Pa,

Business Insurance Harrisburg Pa,

Business Insurance York Pa,

Commercial Insurance Allentown PA,

Commercial Insurance Lancaster PA,

Commercial Insurance Harrisburg PA,

Landlord Insurance,

Landlord Insurance Reading PA,

Landlord Insurance Berks County,

Commercial Insurance,

Commercial Insurance Reading PA,

Business Insurance Allentown PA,

Commercial Insurance Philadelphia PA,

Commercial Insurance York PA,

commercial property insurance,

Commercial Insurance Berks County

Yes, Workers Compensation Insurance Can be Costly, but Don't Cheat

Providing workers compensation insurance for employees can be a significant expense, especially in industries prone to serious injuries, such as those requiring heavy or potentially dangerous machinery. While some employers may be tempted to misclassify workers as independent contractors rather than as employees in order to avoid worker’s comp insurance and other costs, the penalties for misclassifying employees as independent contractors can be severe.

Providing workers compensation insurance for employees can be a significant expense, especially in industries prone to serious injuries, such as those requiring heavy or potentially dangerous machinery. While some employers may be tempted to misclassify workers as independent contractors rather than as employees in order to avoid worker’s comp insurance and other costs, the penalties for misclassifying employees as independent contractors can be severe.

IRS Guidelines for Determining Independent Contractor Status

According to the IRS:

You are not an independent contractor if you perform services that can be controlled by an employer (what will be done and how it will be done). This applies even if you are given freedom of action. What matters is that the employer has the legal right to control the details of how the services are performed.

Consequences of Treating an Employee as an Independent Contractor

If you classify an employee as an independent contractor, whether to avoid workers compensation costs or purely by accident, and you have no reasonable basis for doing so, you may be held liable for employment taxes for that worker as well as incur severe penalties. See the IRS guidelines for determining employee vs. independent contractor status for more information.

Some Common Sense Guidelines for Determining Independent Contractor Status

While the IRS provides detailed guidelines for determining independent contractor status, it may be helpful to consider how one state simplified the criteria. New York State noted these requirements to be eligible for independent contractor status:

- Advertising

Has his/her own advertising (business cards, commercials, phone book listing, etc.)

- Authority

Performs work via his own contract, permit, or authority

- Control

Controls the manner and time for work performed

- Different Work and Customers

Performs work that differs from the primary work of the hiring business, and performs work for other businesses

- EIN or Business Tax Return

Has a Federal Employer Identification Number (EIN) from the Federal IRS or has filed federal business or self-employment income tax returns for work or services performed in the prior calendar year

- Equipment

Provides all equipment and materials needed to perform services under the contract

- Liability Insurance

Has liability insurance (and if appropriate, has worker’s comp and disability insurance policies) under its own business name and Federal EIN

- Obligations

Has recurring business liabilities and obligations

- Profit & Loss

Operates under a specific contract, is responsible for satisfactory performance of work, is subject to profit or loss in performing the specific work under such contract, and is in a position to succeed or fail if the business's expenses exceed income

- Separate

Maintains a separate business establishment

Protecting Your Business from Workers Compensation Insurance Penalties

The above information is intended to be used only as an overview regarding independent contractor status. If you are in doubt as to the status of an independent contractor, seek professional advice from a local tax attorney, or get an opinion from the IRS by filling out form SS-8. The stakes for misclassification can be high, and disputes over worker status can be both expensive and disruptive to your business, sometimes resulting in crippling retroactive penalties.

Get the Right Workers Compensation Insurance Coverage for Your Business

If you would like help in acquiring affordable workers compensation insurance for your business, please Contact Us. Our helpful and courteous team will help you obtain quality insurance coverage at an affordable price. To learn more about workers compensation insurance, please click below.

Tags:

Workers Compensation Insurance,

Business Insurance Reading PA,

Business Insurance Berks,

Business Insurance Philadelphia Pa,

Business Insurance Lancaster Pa,

Business Insurance Harrisburg Pa,

Business Insurance York Pa,

Commercial Insurance Allentown PA,

Commercial Insurance Lancaster PA,

Commercial Insurance Harrisburg PA,

PA Workers Compensation Insurance,

Commercial Insurance,

Commercial Insurance Reading PA,

Business Insurance Allentown PA,

Business Insurance,

Commercial Insurance Philadelphia PA,

Commercial Insurance York PA,

Commercial Insurance Berks County

Use Knowledge to Offset Higher Business Insurance Costs

Having the proper business insurance can be vital to growing your company and protecting your future. While every business varies in terms of exposure to risk and the related cost of coverage, knowing the 5 key cost drivers can help you reduce your insurance costs, whether you are in a mid-sized city like Reading or Allentown, a smaller city like York or Lancaster, or a large city like Philadelphia, especially if you consider costs before launching your business.

Having the proper business insurance can be vital to growing your company and protecting your future. While every business varies in terms of exposure to risk and the related cost of coverage, knowing the 5 key cost drivers can help you reduce your insurance costs, whether you are in a mid-sized city like Reading or Allentown, a smaller city like York or Lancaster, or a large city like Philadelphia, especially if you consider costs before launching your business.

In the end, the cost of business insurance is driven by risk levels as perceived by your insurance carrier, and increases due to higher levels of risk. Regardless of the precise details associated with your business, your costs will be affected by some factors that statistically are related to your company type, company location, and other factors.

Here are 5 Key Drivers of Business Insurance Costs:

#1 - Coverage Level Desired

It goes almost without saying that the cost of your business insurance coverage depends largely on the amount of coverage you desire. It is wise to get the advice of a trusted independent insurance agent before finalizing your coverage level. In some cases you may be able to reduce coverage in a policy if the coverage overlaps with protection already provided in another policy.

#2 - Business Location

Insurance costs may vary widely by state and by city. Businesses located in high-risk areas will pay higher rates. Risk assessments are affected not only by crime rates, but by the likelihood of incurring damage due to storms and other natural disasters. Check with your insurance agent regarding insurance costs prior to relocating your business or purchasing a new property.

#3 - Market

A business in an industry known for high losses will incur higher insurance costs, all else being equal. Industries known for physical risk and high worker's compensation losses will incur higher commercial insurance costs. Expect considerable swings in insurance rates based on the percentage of your employees working in an office setting vs. a construction or other setting known for physical risk.

#4 - Business Insurance Claims History

As with auto insurance and homeowners insurance, businesses also incur higher rates as the frequency of their claims increases. Consider potential cost increases that may result from filing a claim vs. covering the cost out of pocket without filing a claim, especially when you are considering changing insurance carriers.

#5 - Optional Coverage Selected

Although adding optional coverage increases your total insurance bill, optional coverage may be to your benefit. Consider business interruption insurance and key person insurance for executives and others who cannot be easily replaced, and whose absence is likely to cause a slowdown in business.

Do it Right - Get Help

Knowing the key drivers of business insurance costs and planning accordingly can help you navigate your insurance coverage options, and help you achieve the right level of coverage at the right price. Ask your independent insurance agent for assistance in understanding your options and the impact on cost.

We're Ready to Assist You with All Your Business Insurance Needs

American Insuring Group is an independent insurance agency located near Reading, PA, in Berks County. We can help you get the right business insurance coverage for your business at the best price by researching the most affordable insurance costs from our many competing insurance carriers. Contact us today at 800-947-1270 and request a no-obligation, no-cost consultation, or fill out the form on our Contact Us page to get started.

Tags:

Business Insurance Reading PA,

Business Insurance Berks,

Business Insurance Philadelphia Pa,

Business Insurance Lancaster Pa,

Business Insurance Harrisburg Pa,

Business Insurance York Pa,

Small Business Insurance,

Small Business Insurance Reading PA,

Commercial Insurance Allentown PA,

Commercial Insurance Lancaster PA,

Commercial Insurance Harrisburg PA,

Commercial Insurance,

Commercial Insurance Reading PA,

Business Insurance Allentown PA,

Business Insurance,

Commercial Insurance Philadelphia PA,

Commercial Insurance York PA,

Commercial Insurance Berks County

Is Business Insurance Too Complicated?

Business insurance: mention the topic and count down the seconds until yawns form and eyes glass over. For some, commercial insurance is just slightly more interesting than reading the phone book or memorizing the periodic table of elements.

Perhaps that’s because business insurance seems complicated, or because we suspect we’ll never really need it. Talking about what might occur, such as a catastrophe requiring financial assistance, rather than what is likely to occur (business as usual), can seem so abstract, such a waste of time.

3 Things Needed for Entrepreneurial Peace of Mind

Ah, but think of it this way: wouldn’t it be great to have the peace of mind of knowing that you are financially covered against many of the uncertainties life can throw at you? Isn’t that better than the nagging feeling that you may be unprotected against some unknown liability for which you failed to get the needed business insurance protection?

Ah, but think of it this way: wouldn’t it be great to have the peace of mind of knowing that you are financially covered against many of the uncertainties life can throw at you? Isn’t that better than the nagging feeling that you may be unprotected against some unknown liability for which you failed to get the needed business insurance protection?

To get to that blissful entrepreneurial state of mind, you need 3 simple things, none of which require yoga classes or the help of a Zen master:

- Knowledge of basic business insurance terms and types of protection

- A trustworthy and capable independent business insurance advisor

- Decisiveness

Get all three, and in no time you’ll be covered with the right business insurance protection. Whether your business is in Reading, PA, Berks County, Philadelphia, Lancaster, Allentown, or beyond, every business owner who meets those 3 simple criteria sleep better at night.

Buiding Your Business Insurance Knowledge: 14 Terms You Need to Know

While we can’t cover everything you need to know in this short post, we can get you started by presenting 14 key commercial insurance terms, each with a brief definition, in alphabetical order. Read over them and then jot down some follow up questions for your independent insurance agent. Once you have solidified your knowledge, decisiveness will follow. Take action for the good of your business, your employees, and your family.

- Bonding

A guarantee of performance required for many businesses, and often by general contractors, janitorial companies, and businesses with government contracts

- Broker

An independent insurance agent who represents multiple insurance companies, and is therefore in a better position to find the right business insurance at the right price vs. a single-company insurance salesman

- Business Interruption Insurance

Coverage to replace lost sales and income suffered due to a covered loss

- Direct Writer

The opposite of a broker, a direct writer represents a single insurance company

- Disability Insurance

Insurance that pays a fixed monthly benefit if one becomes disabled and unable to perform their regular job

- Employment Practices Liability Insurance

Coverage that protects the business from being sued due to the actions of employees, such as discrimination, abuse, sexual harrassment or wrongful termination

- Errors and Omissions Liability Coverage

Protection for accountants, consultants, and other business professionals against damages due to an error or omission in work performed

- General Liability Insurance

Business insurance protection against accidents of bodily injury or property damage to other persons or property

- Key Person Insurance

Life insurance taken out against a key person, typically an executive or other key person, with the business itself as the beneficiary

- Package Policy

A business insurance policy combining several types of protection in one package

- Property Insurance

Protects equipment and other physical property from losses due to fire, theft, and other incidents, and is available in the form of “named peril” and “all risk” versions

- Replacement Cost Insurance

Insures the business for the full current replacement cost

- Umbrella Coverage

Liability insurance protection for amounts exceeding coverage on main policies, in the event a lawsuit exceeds underlying limits of coverage

- Worker’s Compensation Insurance

Business insurance for medical, rehab, and lost wages for employees who are injured at work (usually state mandated)

There you have it. 14 simple business insurance terms that probably have you wondering what coverage you are missing, and ready to contact your independent insurance agent. Do that, and then get ready to be decisive. You’re almost there.

How to Get Help with Your Business Insurance

Need help in figuring out the right commercial insurance protection for your Reading PA, Berks County, Philadelphia, Allentown, or Lancaster County business? Call us today at (800) 947-1270 for a free consultation, or click to contact us.

Tags:

Business Insurance Reading PA,

Business Insurance Berks,

Business Insurance Philadelphia Pa,

Business Insurance Lancaster Pa,

Business Insurance Harrisburg Pa,

Business Insurance York Pa,

Small Business Insurance,

Small Business Insurance Reading PA,

Commercial Insurance Allentown PA,

Commercial Insurance Lancaster PA,

Commercial Insurance Harrisburg PA,

Commercial Insurance,

Commercial Insurance Reading PA,

Business Insurance Allentown PA,

Business Insurance,

Commercial Insurance Philadelphia PA,

Commercial Insurance York PA,

Commercial Insurance Berks County

Are You at Risk?

Are You at Risk?

Even if you have good automobile and homeowner’s insurance, you may be liable for excessive damages resulting from a major lawsuit. Consider what would happen if you were to injure a doctor, lawyer, or other highly paid professional in a car or other accident that prevented him from earning his regular income for the rest of his life. A court could easily award damages far exceeding the limits of your auto, watercraft, or homeowner’s insurance policy. Such damages could drastically alter your lifestyle for many years to come.

That’s where umbrella liability insurance comes in. The right policy will provide the additional protection needed to withstand such an event.

You May be at Higher Risk for a Lawsuit

Higher-income individuals who cause an accident have a far greater risk of being sued as lawyers seek out those with deep pockets. In such cases an umbrella policy may provide the protection that could be the difference between maintaining your lifestyle vs. paying punitive damages out of pocket for the rest of your life.

An Umbrella Liability Policy May be More Affordable Than You Think

Umbrella liability insurance tends to be more affordable than other types of insurance because it comes into play only after your other insurance has been exhausted. For example, a $1,000,000 umbrella policy would cover up to an additional $600,000 of protection on a homeowner’s policy with $400,000 of coverage. The same principle applies to automobile and watercraft insurance. Increased savings may be found by purchasing your umbrella policy from the same insurance provider as for your home, car, commercial property, or watercraft.

Commercial Property and Umbrella Insurance

Are you a business owner or landlord? If so, you are at greater risk of incurring a lawsuit. Landlord insurance in the form of an umbrella liability policy can provide additional protection against lawsuits from tenants, as well as from being sued for slander or libel by disgruntled employees.

Do You Have an Adequate Umbrella Policy?

If you would like help in obtaining the right level of insurance protection then please click to contact us, or call us at 800-947-1270.

Tags:

Umbrella Liability Insurance,

Homeowners Insurance Lancaster Pa,

Homeowners Insurance Philadelphia Pa,

Small Business Insurance,

Small Business Insurance Reading PA,

Landlord Insurance,

Car Insurance,

Homeowners Insurance,

Homeowners Insurance Allentown Pa,

Homeowners Insurance Reading Pa,

Homeowners Insurance Harrisburg PA,

Homeowners Insurance York PA,

Umbrella Insurance,

Commercial Insurance,

Business Insurance

Landlord Insurance Basics

Landlord Insurance Basics

Landlord insurance is designed to protect the landlord from incurring losses on his or her rental properties. This ranges from property damage to court/legal costs and more, including loss of rental income from a property that becomes inhabitable due to storm damage or other causes.

Do You Need Landlord Insurance?

Does life throw unexpected circumstances our way? If you are a landlord, then of course you need landlord insurance. The question is not whether you need it, but what types of coverage and how much of each type you need. For example, with lawsuits rampant in today’s society, it is wise to consider coverage for discrimination and slander, even if you are certain that you would never commit either. To sleep better at night you may even want to consider comprehensive coverage, which protects you against circumstances not specifically identified in your policy.

Your Property is a Major Investment. Treat it as Such.

Would you go without homeowners insurance or car insurance? Then why consider going without landlord insurance? Your rental property value may easily eclipse your home value, and a loss of your rental property due to fire, storm damage, or other factors can lead to a long-lasting financial upheaval and loss of cash flow that can be easily avoided with the proper insurance coverage.

Not All Landlord Insurance is Created Equal

It is important for landlords to understand exactly what is and what is not covered under their policy. Policies may vary widely, so be sure to work with your insurance agent to understand all the important aspects of your current coverage and to uncover your potential vulnerabilities. For example, your policy may cover only certain types of damage, such as exterior vs. interior damage. Likewise, legal costs may be excluded from your policy. Be sure to ask your independent insurance agent what types of additional coverage are available from your current carrier and from competing insurance carriers, and then consider switching carriers or upgrading your policy if needed. Your independent insurance agent represents multiple insurance companies, so changing to another carrier is easy with the right agent.

Need Help Understanding Your Landlord Insurance Options?

Contact us today for a free evaluation: 800-947-1270

Tags:

Business Insurance Berks,

Small Business Insurance,

Small Business Insurance Reading PA,

Commercial Insurance Allentown PA,

Commercial Insurance Lancaster PA,

Commercial Insurance Harrisburg PA,

Landlord Insurance,

Insurance Reading Pa,

Landlord Insurance Reading PA,

Landlord Insurance Berks County,

Commercial Insurance,

Commercial Insurance Reading PA,

Business Insurance,

Commercial Insurance Philadelphia PA,

Commercial Insurance York PA,

commercial property insurance,

Commercial Insurance Berks County