Have you ever wondered what factors determine your life insurance rates? Is it just your age…the state of your current health? Is there anything you can do to make your life insurance more affordable?

Have you ever wondered what factors determine your life insurance rates? Is it just your age…the state of your current health? Is there anything you can do to make your life insurance more affordable?

Insurance companies look at several factors to determine the likelihood that A) you’ll live a very long life, or B) you’ll die very soon. As depressing as that may sound, it’s a fact, and it’s what determines your life insurance premium.

What Do Life Insurance Companies Consider When Setting Your Premium?

While every insurance company has its own underwriting criteria to determine your premium, you may be surprised by some of the factors they look at. What isn’t surprising is that many of the factors that determine your life insurance premiums can also affect the quality and/or length of your life. Some you can change and some you can’t.

Here are eight factors many insurance companies use to determine your life insurance premiums, and some tips on how to get a better rating and save on your life insurance policy.

1. Driving violations

If you’ve had two moving violations in the past year or a DUI in the past 5 years, you may be considered a reckless driver, which could put your life in danger and pose more risk for the insurance company. There isn’t much you can do about existing violations, but you can SLOW DOWN and not drink and drive.

2. Your workplace colleagues

If you have group life insurance from your workplace, the premiums are based on the average age and health of everyone, not just you. So if you work with a group of individuals who are older and less healthy than you, it may raise your premium. On the other hand, if you work with a group of individuals who are younger and healthier than you, it may lower your premium. Make sure you compare the price of an individual health insurance policy before jumping into a group plan.

3. Credit history

Individuals who have filed for bankruptcy are considered a high-risk proposition and many insurance companies won’t even issue a policy until their credit report has been cleared. Make sure you consider all the alternatives and consequences before filing for bankruptcy.

4. Lifestyle

Are you a daredevil? Do you prefer skydiving to reading…car racing to gardening? Certain hobbies can disqualify you from getting the best rate on life insurance. Even travel outside of the country can increase your premiums. So, consider the increased cost of life insurance when weighing the pros and cons of your career choices.

5. Occupation

Higher-risk occupations, such as airline pilots and high-rise construction engineers, can create a higher risk for premature death, thereby causing higher life insurance premiums. Solution – choose your occupation wisely.

6. Smoking Habits

We all know smoking can raise your risk of stroke, lung disease and many other life-threatening medical conditions; therefore insurers often charge smokers a higher premium. One more reason to kick the habit.

7. Your weight

There are a number of diseases related to being overweight that can shorten your lifespan. Most insurers look at height, weight, and body mass index (BMI) to determine your premium. Plus, many insurers want to see you keep that weight off for at least one year before they will offer you a better rate. So if you were looking for that final push to get you started on an exercise and diet plan, think about all the money you can save on your life insurance premiums.

8. Family health history

Your family’s medical history shows what diseases you may be prone to. You can choose your friends, but not your family; however, you can choose to protect your family with the right level of life insurance, and you can ask your doctor for advide on how you may be able to reduce your health risks through proper diet, exercise, and other factors in light of your family medical history.

Ready to Talk Life Insurance?

Ready to Talk Life Insurance?

Contact American Insuring Group at (800) 947-1270 or (610) 775-3848 to learn more about your life insurance options, or for a free quote on life insurance.

Do you believe that your employees are one of your most valuable assets? Do you think of your employees as an investment rather than an expense?

Do you believe that your employees are one of your most valuable assets? Do you think of your employees as an investment rather than an expense?  Contact American Insuring Group

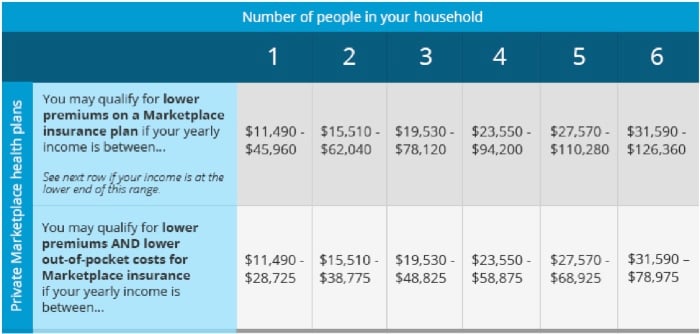

Contact American Insuring Group There is a lot of uncertainty these days regarding what is required under the Affordable Care Act, also known as ObamaCare. Businesses and individuals alike are concerned they may be penalized or miss out on important information needed to keep their

There is a lot of uncertainty these days regarding what is required under the Affordable Care Act, also known as ObamaCare. Businesses and individuals alike are concerned they may be penalized or miss out on important information needed to keep their

If your business requires the use of heavy equipment - such as tractors, backhoes, and forklifts – chances are a large percentage of your business assets are tied up in that equipment, making the protection of that equipment from damage or loss a high priority for you and your business.

If your business requires the use of heavy equipment - such as tractors, backhoes, and forklifts – chances are a large percentage of your business assets are tied up in that equipment, making the protection of that equipment from damage or loss a high priority for you and your business.  Since no amount of prevention will stop every thief, it’s important that you contact an American Insuring Group agent at

Since no amount of prevention will stop every thief, it’s important that you contact an American Insuring Group agent at  A new year is a great time for reflection and fresh starts. It’s the perfect time to put the past behind you and look toward the future. Compared to losing those extra 20 pounds, protecting your family in the event of a death is a surprisingly easy New Year’s resolution.

A new year is a great time for reflection and fresh starts. It’s the perfect time to put the past behind you and look toward the future. Compared to losing those extra 20 pounds, protecting your family in the event of a death is a surprisingly easy New Year’s resolution.  Looking to the future by protecting your family with life insurance is one of the easiest and most selfless resolutions you can make. Make it a goal to protect your family with the right life insurance.

Looking to the future by protecting your family with life insurance is one of the easiest and most selfless resolutions you can make. Make it a goal to protect your family with the right life insurance.  Be honest! Did you make any New Year’s resolutions this year? If you did, you weren’t alone. According to Statistic Brain, 45% of Americans “usually” make New Year’s resolutions, and according to Constant Contact®, 53% make business-related resolutions.

Be honest! Did you make any New Year’s resolutions this year? If you did, you weren’t alone. According to Statistic Brain, 45% of Americans “usually” make New Year’s resolutions, and according to Constant Contact®, 53% make business-related resolutions.

e’ve all heard stories about celebrities insuring various body parts for ridiculous sums of money - most famously, Betty Grable’s legs were insured for a million dollars. Why would anyone insure such a thing? The fact of the matter is, her studio made a lot of money off of Betty Grable’s appearances, and a large part of her appeal were her fabulous gams. If her legs had been marred in any way, her ability to sell movies and posters would’ve been greatly reduced.

e’ve all heard stories about celebrities insuring various body parts for ridiculous sums of money - most famously, Betty Grable’s legs were insured for a million dollars. Why would anyone insure such a thing? The fact of the matter is, her studio made a lot of money off of Betty Grable’s appearances, and a large part of her appeal were her fabulous gams. If her legs had been marred in any way, her ability to sell movies and posters would’ve been greatly reduced.  If you have people who are as valuable to your business as Betty Grable’s legs were to her,

If you have people who are as valuable to your business as Betty Grable’s legs were to her,

Do you want to become a burden to your family? Of course not.

Do you want to become a burden to your family? Of course not. If you want to ensure that you can live independently and not become a burden to your family and friends in the event that you need care over a long period of time, give us a call at

If you want to ensure that you can live independently and not become a burden to your family and friends in the event that you need care over a long period of time, give us a call at  While most Pennsylvania homes and businesses are not considered to be in a flood plain, that doesn't mean that buildings in Pennsylvania don't flood. Even low risk areas suffer flooding due to poor drainage systems, blockages, broken mains, or rapid precipitation. The average homeowner's and business insurance does not cover flood damage, so it merits a discussion whether to purchase a flood insurance policy to protect yourself.

While most Pennsylvania homes and businesses are not considered to be in a flood plain, that doesn't mean that buildings in Pennsylvania don't flood. Even low risk areas suffer flooding due to poor drainage systems, blockages, broken mains, or rapid precipitation. The average homeowner's and business insurance does not cover flood damage, so it merits a discussion whether to purchase a flood insurance policy to protect yourself. So don’t wait until you see the ark float by; find out what kind of flood insurance works for you to protect your home and business! Give us a call at

So don’t wait until you see the ark float by; find out what kind of flood insurance works for you to protect your home and business! Give us a call at  Workers' Compensation Insurance and Minimum Wage Increases

Workers' Compensation Insurance and Minimum Wage Increases